The Real Currency of Media M&A: How IP Powerhouses Are Reshaping Content Empires

- Isheta T Batra, Kanika Goswamy

- Feb 28

- 9 min read

You’ve probably seen the headlines about Warner Bros. Discovery getting snapped up by Paramount Skydance for $110 billion, right after Netflix backed out of its $82.7 billion offer. Beyond the drama of competing offers lies a pivotal industry truth: intellectual property (IP) now drives media mergers more than cash, infrastructure, or subscriber counts. This shift creates both challenges and unprecedented opportunities particularly for Indian platforms, creators, and investors navigating global content flows.

The question analysts are debating: why did bids differ by $27 billion? The question they should be asking is far more fundamental i.e. what exactly were they bidding for? The answer is not studios. Not distribution infrastructure. Not even subscriber bases. They were bidding for intellectual property: the DC Universe, Game of Thrones, Harry Potter, The Matrix, CNN's archive, Paramount's century-old film library. The physical assets like the lots, the offices, the servers, are incidental. The IP library is the empire.

This episode, dramatic as it is, is merely the most visible symptom of a structural transformation that has been reshaping media M&A for nearly a decade. Intellectual property has quietly displaced every traditional asset class as the dominant variable in media valuation. And for Indian platforms, Indian creators, and Indian content businesses operating within global licensing ecosystems, this transformation carries profound and underappreciated consequences.

How IP Became the Balance Sheet

For most of the 20th century, media M&A valued physical and operational assets: broadcast towers, production infrastructure, distribution networks, and advertiser relationships. Content was important but depreciating; a film earned its money in theaters, then faded. The streaming era broke this model irreversibly.

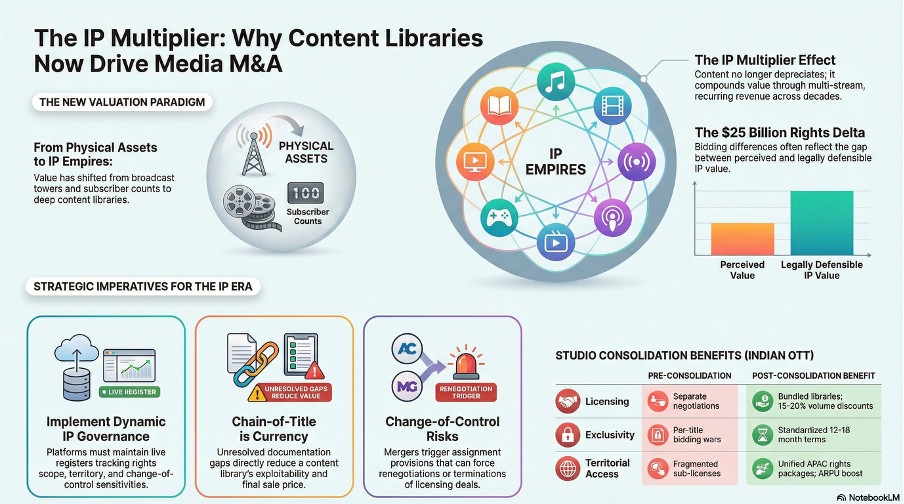

When Netflix paid $100 million to retain Friends for a single year (2019), it signaled a new paradigm: content does not depreciate in the streaming economy; it compounds. Catalog titles generate subscriber retention, reduce churn, and anchor platform identity across decades. A single franchise like Harry Potter does more than generate box office revenue. It produces theme park licensing, publishing rights, gaming adaptations, merchandise, experiential content, and perpetual streaming value simultaneously, across territories and over decades.

This is what financial analysts call the IP Multiplier Effect: the capacity of a single content asset to generate recurring, non-correlated, multi-stream revenue indefinitely. Traditional EBITDA-based valuation models treat IP libraries as static assets on a balance sheet. In reality, they function more like equity portfolios—dynamic, compounding, and appreciating with cultural relevance rather than depreciating with time. The data supports this emphatically.

Disney's acquisition of 21st Century Fox (2019, $71 billion) was justified largely on the strength of the Marvel and X-Men IP additions, not Fox's studio infrastructure.

Amazon's $8.5 billion acquisition of MGM (2022) was widely described by analysts as "buying James Bond and Rocky."

AT&T's acquisition of Time Warner was, at its core, a bid for DC Comics and HBO's prestige library.

In every major media deal of the past decade, the IP library dictated the floor valuation; everything else negotiated around it. The Warner-Paramount deal is simply the most explicit articulation of this logic yet. Netflix's bid was superior on cash liquidity. Paramount's winning structure was superior on IP integration and long-tail exploitation. The board chose IP upside over immediate cash, and in doing so, confirmed that IP is no longer a component of media valuation. It is the valuation.

The Legal Architecture of IP Value And Why It Is Routinely Underestimated

Here is where the legal dimension becomes critical, and where most business analysis falls short. IP in media is not a clean asset. It is a layered, fragmented, jurisdictionally complex web of rights, and the gap between the perceived value of an IP portfolio and its legally defensible value is often enormous.

Consider how rights actually sit inside a major studio library:

Chain of Title Fragmentation:

A single film may involve the original author's heirs (moral rights, reversion claims), co-producers (revenue participation, sequel rights), distributors (territorial exclusives), music rights holders (synchronization licenses), and writers (guild residuals). Each layer is a potential dispute point. Each gap in the chain reduces exploitability. A studio may market 5,000 titles in its library, but if 800 of them carry unresolved chain-of-title defects, that premium valuation rests on shaky foundations.

Reversionary Rights:

Under both U.S. copyright law (35-year termination rights) and international equivalents, original creators retain the right to reclaim IP assignments after a statutory period. This creates a ticking clock on major catalog assets that acquirers frequently undervalue during diligence. For the current WBD portfolio, a meaningful percentage of pre-1990 catalog faces reversionary exposure in the coming decade, a liability that sophisticated acquirers must price.

Territorial Licensing Conflicts:

Studios historically licensed IP territory-by-territory, creating a global patchwork of exclusivities, holdback periods, and sub-distribution arrangements. A merged entity that seeks to exploit IP globally through a unified streaming platform runs directly into these agreements. Consolidating rights from this patchwork requires renegotiation, buyouts, or litigation, all costly and time-consuming.

Moral Rights and Author Protections:

In jurisdictions that recognize moral rights (including India under Section 57 of the Copyright Act, 1957), authors retain rights to integrity and attribution regardless of economic ownership transfer. A new parent entity cannot simply reboot, adapt, or modify acquired IP without navigating the original creator's moral rights, a constraint that materially limits exploitation flexibility.

These are not academic legal footnotes. They are the difference between a $110 billion library and an $85 billion one. The $25 billion delta in competing bids is, in significant part, a function of how each party's legal team assessed these exposures.

Indian Media in a World Owned by IP Gatekeepers

India is not a passive observer in this consolidation. It is a deeply integrated participant — and one of the most exposed markets globally to the disruption that IP-driven consolidation creates.

Indian OTT platforms like JioCinema, Disney+ Hotstar, SonyLIV, Zee5, and emerging players have built significant portions of their premium content catalogues on licensed Hollywood IP. HBO's House of the Dragon, Paramount's Yellowstone, DC franchise films — these titles drive subscription conversions, premium pricing, and viewer retention in the Indian market at a scale that domestic originals alone cannot yet match.

Consolidation streamlines this ecosystem without foreclosing growth:

Licensing Dynamic | Pre-Consolidation | Post-Consolidation Benefit | Indian Platform Impact |

Output Deals | Separate negotiations with WBD/Paramount | Bundled HBO + Paramount libraries | Volume discounts (15-20% savings, Reliance-Viacom precedent); predictable pricing |

Exclusivity Windows | Per-title bidding wars | Standardized 12-18 month terms | Reduced competition; Hindi-dubbed premiums locked at scale |

Territorial Access | Fragmented sub-licenses | Unified APAC rights packages | Full catalog access (vs. selective titles); ARPU boost from $2 to $4+ |

MFN Protections | Studio-specific clauses | Cross-library parity | Jio/Disney-scale leverage flows to mid-tier (SonyLIV, Zee5) |

When the ownership structure of that IP changes, every downstream agreement built on it is stress-tested.

What Actually Happens to an Indian Platform's Licensing Deal When Studios Merge

A licensing agreement between an Indian OTT and Warner Bros. Discovery contains a contractual counterparty, WBD. When Paramount acquires WBD, the contracting entity changes. How that plays out legally depends entirely on the specific provisions of each agreement, and the gap between well-drafted and poorly-drafted contracts becomes financially material at scale.

Change of Control Clauses:

Sophisticated licensing agreements include provisions that either (a) allow the licensee to terminate if the licensor undergoes a change of control, or (b) allow the new parent to renegotiate. Poorly drafted agreements may simply continue under assignment, at whatever commercial terms the original deal specified, even if market rates have shifted dramatically. Indian platforms with long-term output deals signed at 2020-era pricing may find themselves locked in advantageously, or exposed to clawback arguments, depending on exact drafting.

Assignment Provisions:

Many content licenses prohibit assignment to third parties without consent. A merger technically triggers an assignment of the licensor's obligations to the surviving entity. Indian platforms that signed agreements without robust anti-assignment protections may face demands for consent fees, renegotiation pressure, or even termination threats from the new parent asserting consolidation rights.

Most-Favoured Nation (MFN) Clauses:

Output deals frequently include MFN provisions: if the licensor grants a better rate to any other platform, the MFN holder gets the same. Post-merger, a consolidated entity offering preferential terms to a global partner (say, a Jio-level deal) may trigger MFN rights for smaller platforms, or conversely, the new entity may claim the consolidation voids prior MFN commitments. Either outcome creates litigation exposure.

Profit Participation Agreements:

Indian producers and writers involved in co-production deals with WBD or Paramount entities carry contractual profit participation rights. When parent entities merge, financial reporting structures change, and the pools against which participation is calculated can shift. Without explicit protections in the original agreement, these rights can be eroded through legitimate corporate restructuring, a risk that co-producers rarely anticipate during the euphoria of deal-signing.

The CCI Question: Does India Have a Framework for IP-Driven Consolidation?

India's Competition Commission of India (CCI) is equipped to review mergers exceeding prescribed financial thresholds. But its analytical framework for media M&A, as demonstrated in the Star-Disney and Reliance-Viacom18 reviews, focuses predominantly on distribution market share and subscriber overlap. IP concentration as an antitrust harm remains underdeveloped in Indian competition jurisprudence.

This is a significant gap. When a single merged entity controls 40-45% of premium Hollywood IP licensed into India, the competitive harm is not primarily in distribution (Indian platforms remain distinct competitors); it is in upstream content access. If the IP gatekeeper can bundle, exclude, or price-discriminate across Indian platforms, smaller players face foreclosure not through acquisition but through content starvation.

This is the same theory of harm that DOJ litigated in Penguin Random House-Simon & Schuster, and that EU regulators are now developing in digital content markets. Indian competition law is structurally capable of adopting this framework under Section 3 (anti-competitive agreements) and Section 4 (abuse of dominance), but proactive enforcement has lagged.

The Paramount-WBD deal, as it works through global regulatory processes, offers Indian policy makers a rare window to develop clear guidelines on IP concentration in content markets, before a future domestic consolidation makes the absence of doctrine costly.

Indian Creators: The Overlooked Vulnerability

The analysis above focuses on platforms. But the more structurally vulnerable stakeholders are individual Indian creators like writers, directors, composers, and producers who have entered co-production or co-financing arrangements with WBD or Paramount entities over the past five years.

India's OTT boom generated dozens of such arrangements: Indian production houses co-producing English-language content for HBO, licensing music catalogues to Paramount, or entering format-adaptation agreements for scripted content. These deal structures were negotiated when both studios were independent entities, often without adequate provisions for:

Assignment of obligations post-merger

Approval rights over new parent's exploitation strategies

Moral rights protections under Indian Copyright Act, Section 57

Currency and repatriation structures for profit shares under FEMA

Governing law and dispute resolution in the event of counterparty restructuring

A merged entity with consolidated IP strategy may deprioritize or restructure these mid-tier arrangements. Creators who lack robust contractual protections, particularly step-in rights, termination for convenience, and explicit sequel/derivative rights carve-outs, face exposure.

The Structural Takeaway: IP Governance Is Now a Business Priority

The Paramount-WBD deal crystallises a reality that every media businessfrom global studios to regional OTTs to independent Indian production houses must now internalize: IP governance is not a legal function. It is a business strategy.

What does this mean operationally?

For platforms: The value of a content licensing portfolio is only as strong as the clarity of rights underlying it. Platforms should maintain dynamic IP registers: live documents tracking title-by-title rights scope, territory coverage, holdback periods, expiry dates, and change-of-control sensitivities. The cost of this exercise is marginal. The cost of discovering gaps during a merger negotiation is enormous.

For producers: Chain-of-title documentation is a prerequisite for professional content development, not a post-production formality. Every gap like a missing assignment from a co-writer, an unregistered music sync license, an unsigned collaboration agreement, is a deduction from the title's exploitability and therefore its value in any future deal.

For investors: Media investment analysis must incorporate IP quality assessment alongside financial metrics. Two studios with identical EBITDA but different IP portfolio quality present radically different risk profiles. The current deal demonstrates that the market now prices this differential at $25 billion and above.

For deal negotiators: Change-of-control protections, anti-assignment clauses, MFN provisions, moral rights carve-outs, and governing law designations are not boilerplate. They are the provisions that determine commercial outcomes when the entity across the table ceases to exist in its current form, which, in the current consolidation environment, is an increasingly likely scenario.

The Decade Ahead

The Paramount-WBD transaction will not be the last mega-deal in media. Apple, Amazon, and Sony remain active acquirers. NBCUniversal faces strategic questions. Indian conglomerates with OTT assets are potential targets in regional consolidation. The IP-driven logic that powered this deal will accelerate globally.

For Indian media stakeholders, the strategic imperative is clear. The global content market is shifting toward a gatekeeper structure where a handful of entities with dominant IP libraries set the terms for everyone else. Platforms that build IP ownership not just licensing build resilience. Creators who protect rights through disciplined contracting retain leverage. Investors who assess IP quality alongside financials identify value others miss.

The era of media valuation driven by subscriber counts and quarterly revenues is ending. The era of IP as the foundational economic asset has arrived. The $110 billion question is whether Indian media across platforms, production, and policy has positioned itself to compete within it.